This post originally appeared on SynBioBeta on February 26th, 2014

Dr. Jamie Bacher is the founder and CEO of Pareto Biotechnologies. He previously served as Deputy Program Manager and led an 80 employee, $100 million project for Total New Energies in their partnership with Amyris to generate biofuels. At Sapphire Energy, he established a technical infrastructure that was critical to Sapphire’s partnership with Monsanto. He similarly led technical efforts at Rincon Pharmaceuticals as the first scientist to focus on whole-cell optimization; efforts which led to a $1 million funding milestone for the company.

—

Synthetic biology has reached a critical juncture. We’re seeing more companies flounder than exit, resulting in the overwhelming conclusion that synthetic biology companies must get products to market quickly in order to be successful. One of the many challenges companies have faced is how to deliver products both quickly and well.

There is a spectrum from market risk (faced by tech startups) to technical risk (generally the challenge for traditional biotech startups). Many synthetic biology companies sit in the middle of the spectrum, exposed to different levels of both market and technical risk. Investors will need new models, financial and heuristic, to evaluate investment opportunities in the rapidly evolving synthetic biology space.

Technical risk is fundamentally different from that of drug discovery for traditional biotech companies: the risk is less about whether a given product could be made at all (although still often a challenge), but whether that product can be made economically. The risk profile is very different from evaluating whether a drug that works in laboratory assays will pass expensive and lengthy clinical trials. Nevertheless, investors can use signals to evaluate technical risk of seed stage synthetic biology companies in much the same way as traditional, drug discovery-oriented biotech. In addition to the actual technical accomplishments of the company, investors can consider:

Consideration 1: Founding team members

Who is on the founding team, and who are the company’s first employees? Some of the typical signals are: what other companies have the team been a part of or founded – do they have lessons learned from multiple companies with relevance to their space – and how did the team generate value for their investors?

Consideration 2: Technical background

Is the company being founded de novo, or is there an intellectual and technical history to the company? The latter situation is common when the company is being spun out of an academic lab, and often comes with intellectual property that an otherwise comparable de novo company cannot match.

Consideration 3: Current investors

If the company already has investors, who are they? How did they evaluate the opportunity? What is their experience with synthetic biology – what is their technical expertise, and what has been the outcome of their previous investments? The founding team addresses the risk of execution, and the company’s IP enables the company to operate with a competitive advantage. Investors will also consider other signals, quantitative and qualitative.

Consideration 4: Business model

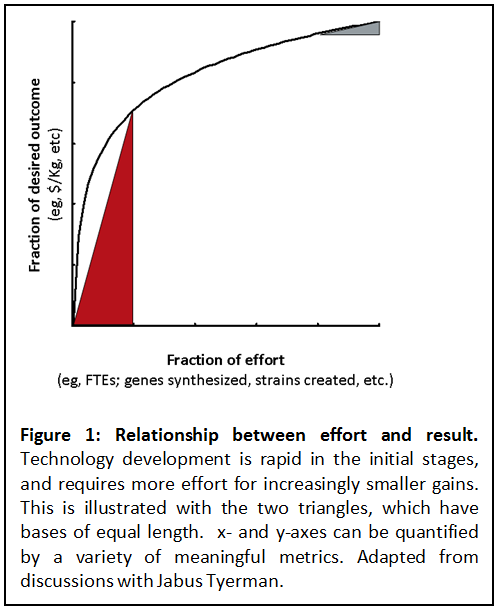

In the past, synthetic biology companies promised to enter trillion-dollar markets, such that capturing a measurable fraction of these markets would guarantee success. Technology development may be worth such investments, but rarely on the timeline that VCs need in order to generate returns for their LPs. A commodity-based business must deliver on 100% of the technology development that is predicted, and hope that all of the assumptions are correct to hit their target. A new business model is developing for synthetic biology companies, which can be described using the 80/20 rule. A company targeting high-value products could require only 20% of the investment, deliver 80% of the technology development, and bring products to market in a reasonable timeframe.

This can be applied as the “Tesla model”: develop the technology by selling a small number of high-priced roadsters, and funnel those funds back into the technology development to deliver a mass-market, reasonably-priced family sedan. Similarly, a synthetic biology company can iterate the process from product to product, in a long-tail model. Each successive, related product after the first one has a progressively lower frictional cost. How does the company plan to leverage its technology from roadsters to sedans? And what are the associated finances.

Consideration 5: Commercialization prospects

How does the company identify and pursue products? Does the company offer a viable and realistic commercialization plan that will ultimately return value to the investor?

Business challenges certainly remain for synthetic biology companies. Acceptance by other industries, where synthetic biology will have impact, has been and will be slower than technologists appreciate, and will advance unevenly within those industries. Regulatory concerns and public opinion must also be addressed.

It is clear that there are opportunities for investors, but these will not follow traditional lines. While this will be a challenge for risk-averse investors, those who are willing to work through these challenges with entrepreneurs will realize the rewards of building an industry as a whole. Synthetic biology investors do not need more opportunities: they need better ones.