Earlier this week, Dealroom released its annual venture capital report (free download), alongside trusted media partner Tech.eu. The report is packed with data and insights. Below are 10 key observations from that report.

Earlier this week, Dealroom released its annual venture capital report (free download), alongside trusted media partner Tech.eu. The report is packed with data and insights. Below are 10 key observations from that report.

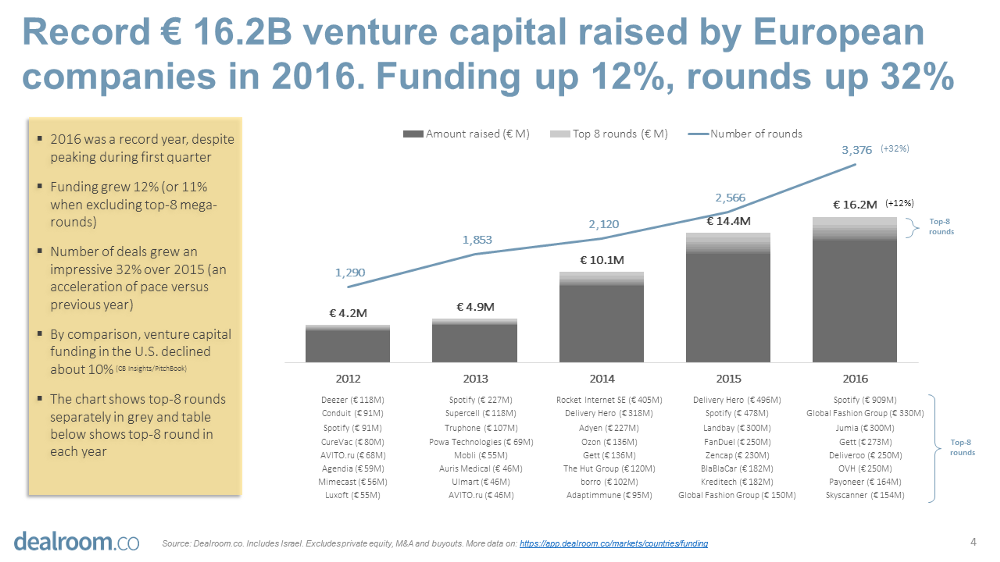

Insight #1: With a record € 16.2 billion raised in 2016, European tech is better capitalised than ever

European companies raised € 16.2 billion (US$ 17.3 billion) in venture capital, an increase of 12% versus the previous year and an all-time record. The number of rounds grew by 32%, from 2,566 to 3,376. By comparison, U.S. venture capital funding was down by about 10% from $ 70-80 billion in 2015 to $ 60-70 billion in 2016. All this despite Europe struggling with a bunch of political and economic upheaval (Brexit, deflation, regional unemployment rates of 12-25%).

As a result, European tech companies in aggregate have more capital at their disposal than ever before, to invest in their product and acquire customers. On the one hand, competition for the same customers will heat up even further, but on the other hand much of Europe is still wide open in terms of the online migration “land-grab”.

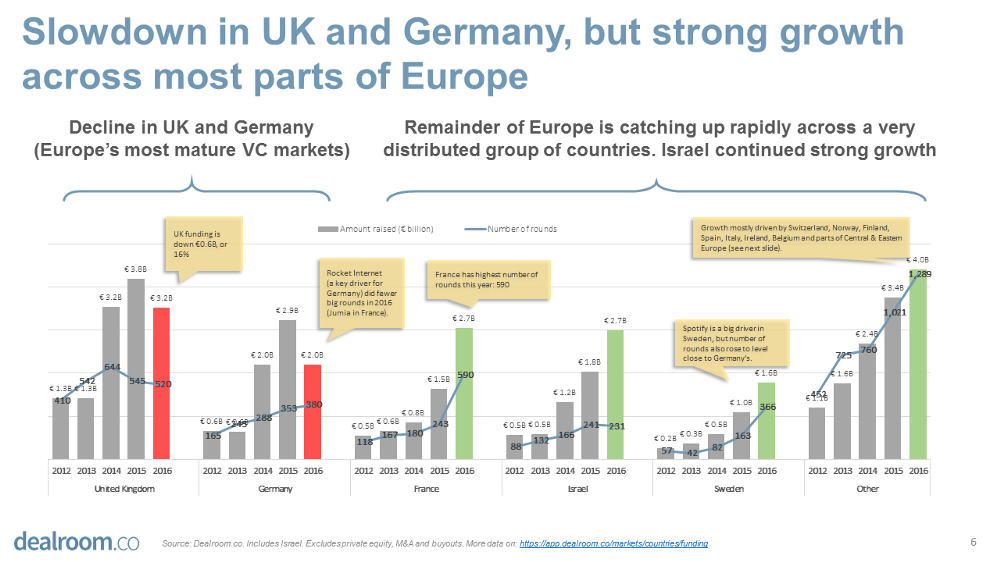

Insight #2: Slow-down in the UK & Germany, France is now leading Europe by number of rounds

Back in 2014 and 2015, the UK and Germany were the torchbearers of European tech, responsible for more than 50% of all European venture capital raised. But in 2016, that percentage fell to 32%. France, Sweden and Israel took the majority of that lost share, while the rest of Europe also did well.

For the first time, France took the #1 spot in terms of number of deals. Is it time for the French to bring out the champagne? Well, why not 🙂 but of course, what’s more important is how these new startups will be able to develop in the coming years. But certainly, it is time for U.S. (and other non-European) funds that have been focusing on the UK and Germany, to widen their horizon.

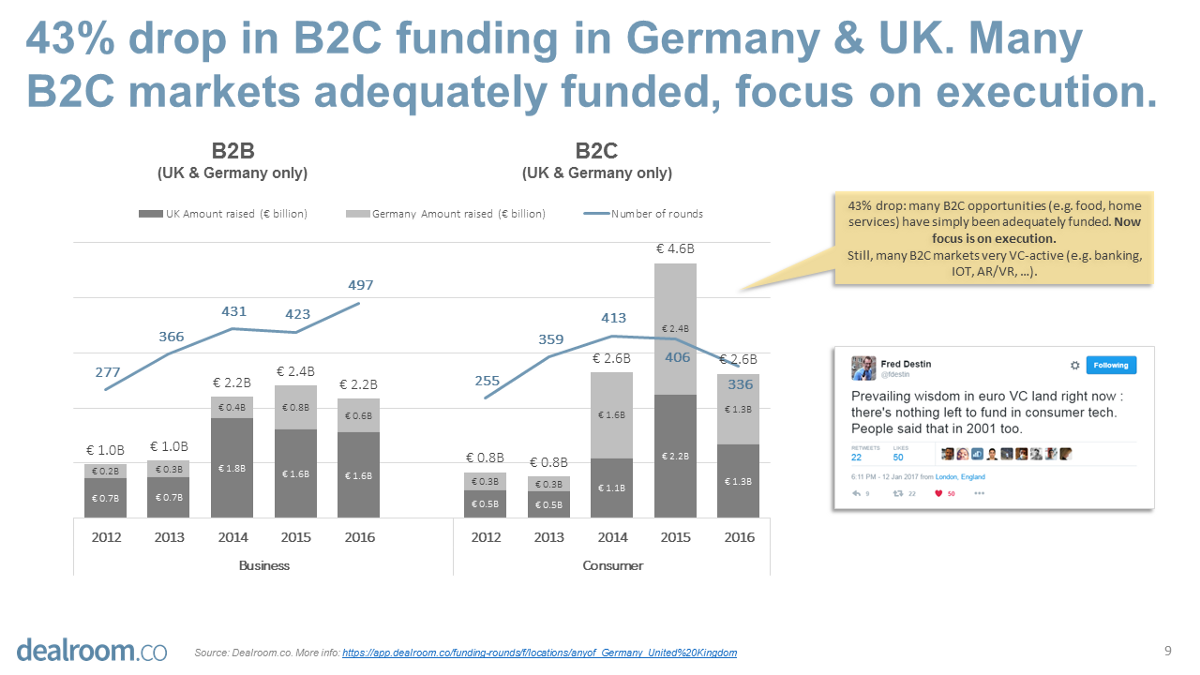

Insight #3: Consumer tech focused more on execution and consolidation in 2016, less on funding

During 2013–2015, a majority of capital went into consumer tech (food delivery, taxis, fashion, home) including well-known UK & German names such as Delivery Hero, Just Eat, Zalando, HelloFresh, Helpling, Home24 home, et cetera. During 2016 these companies focused on execution, consolidation and reaching profitability. This is not a bad thing of course, but the result is a 43% drop in B2C funding in Germany & the UK.

Despite that, over € 7.2 billion (a small increase) was invested in consumer tech in 2016 across Europe. Some top growth categories in consumer tech were: travel, fashion, consumer healthcare, various subscription services and consumer hardware. For 2017, there is plenty of activity to be expected in areas such as consumer banking, Internet of Things, virtual reality, and others.

Another factor explaining the German decline in B2C is that Rocket Internet’s main 2016 funding project was Paris-based Jumia (€ 425 million raised in 2016).

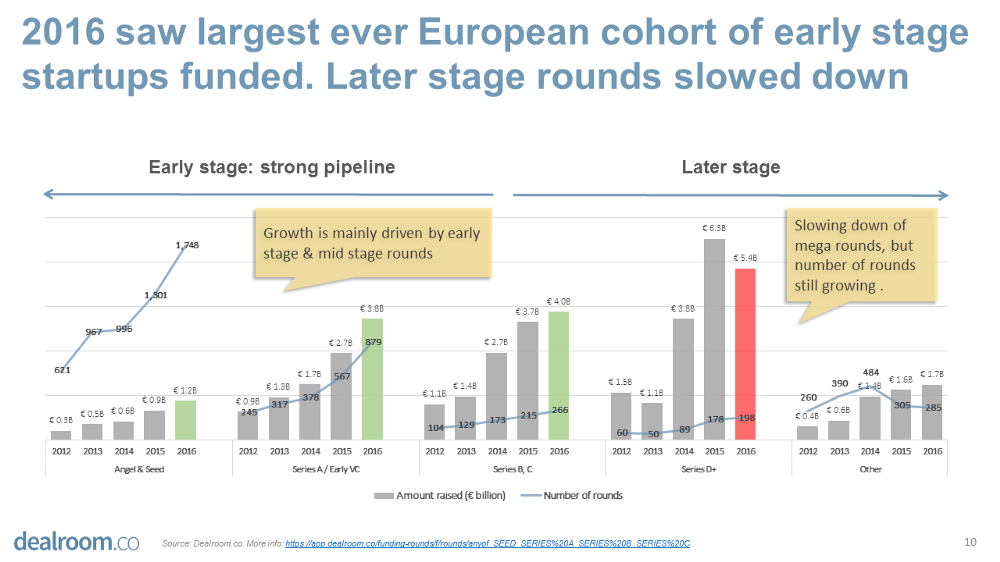

Insight #4: 2016 was the largest ever vintage of European startups

France, Sweden, and many other parts of Europe experienced a surge in number of rounds and total amount raised. Early stage rounds, seed and series-A were key drivers.

France really stood out: the number of seed rounds tripled and early stage rounds doubled, in a nation-wide phenomenon across more than 150 cities. Many French cities saw their first VC round ever in 2016. Several of the most active European investors in 2016 were French (Bpifrance, Kima Ventures, IDInvest, Partech, 360 Capital Partners, BNP Paribas).

By contrast, the total number of seed rounds in the UK declined for two years in a row. Could it be that founders from continental Europe are starting to prefer their home country over London to start a business as local funding options improved? The data doesn’t explain it. But Brexit could push this trend further in 2017: spreading tech hubs across Europe and reducing geographical concentration. There are -no doubt- some pros and cons to this.

One thing is for sure: 2016 is the largest ever vintage (to use a French term) of European early stage startups funded. How bountiful will be the harvest of this 2016 vintage?

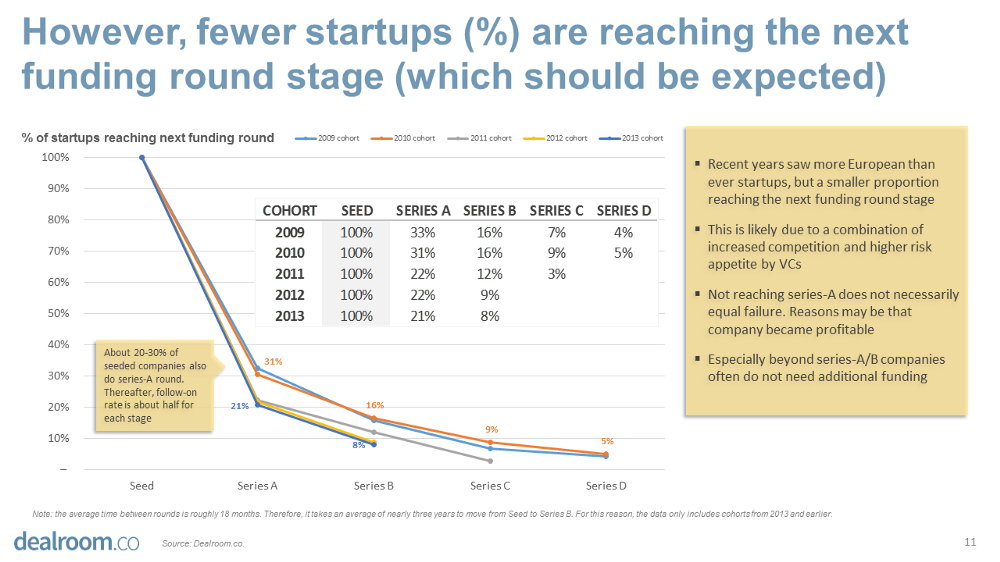

Insight #5: Fewer startups are reaching the next funding stage

While more startups are getting funded, a smaller proportion is reaching the next stage. This may sound alarming, but increased losses is to be expected from increased risk taking — at least to some extent. It also comes with the territory of “embracing failure”, the mantra much heard in 2016.

That said, it’s important to keep a close eye on startup success rates.

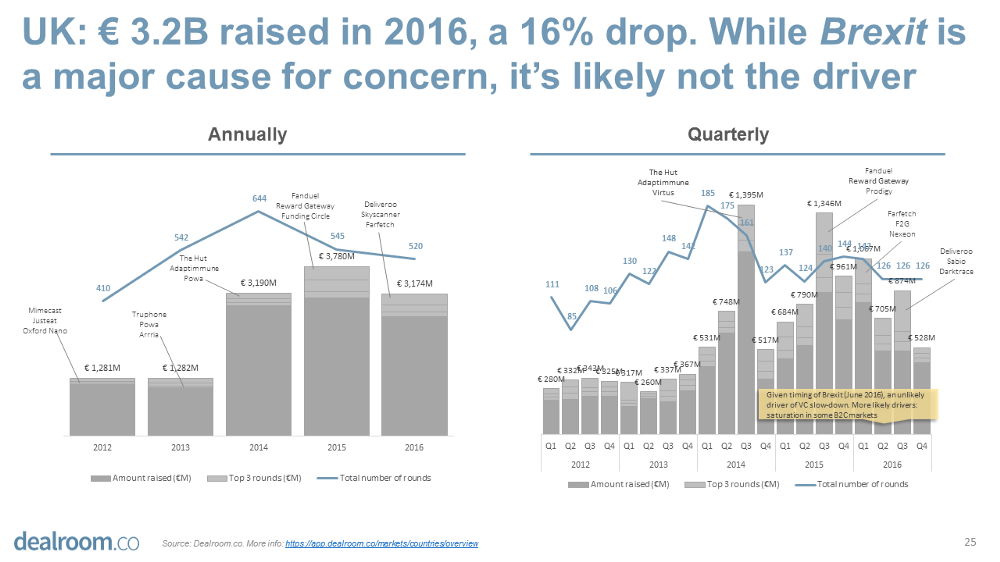

Insight #6: Brexit sucks, but it did not cause a VC slump (yet)

UK venture capital funding dropped by € 600 million (or 16%); the number of UK rounds declined for two years in a row. Commentators suggested more than once that UK funding fell as a result of Brexit. From a timing perspective this is just very unlikely. The slowdown in consumer tech is a much more robust explanation. Commentators are searching for evidence that Brexit was a bad idea (which it was), but unfortunately populist policies often (if not mostly) cause short-term stimulus. The long-term ramifications of the (hard) Brexit have yet to play out.

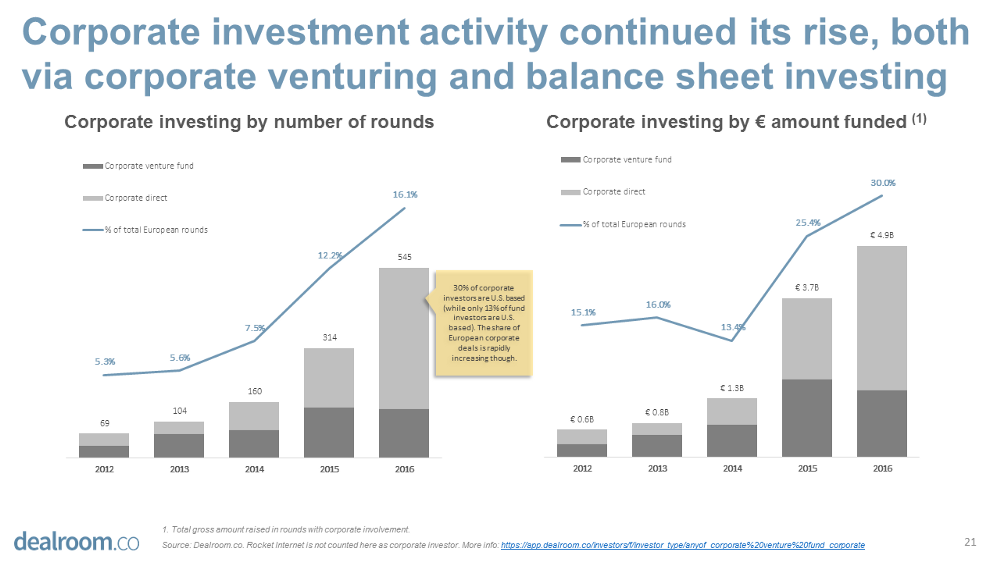

Insight #7: € 4.9 billion in corporate investing, kind of a big deal…

Corporate rounds grew by 33% to € 4.9 billion (that’s the combined size of all VC rounds involving at least one corporate). Even more impressive: the number of rounds grew by 74% to 535 rounds (that’s 16% of all rounds).

These corporates are mostly investing directly from their balance sheet, but also via corporate venture funds (see chart below). Increasingly, corporates also participate in smaller rounds. At the same time, the corporate accelerator model has come under increased criticism from serial founders and angel investors.

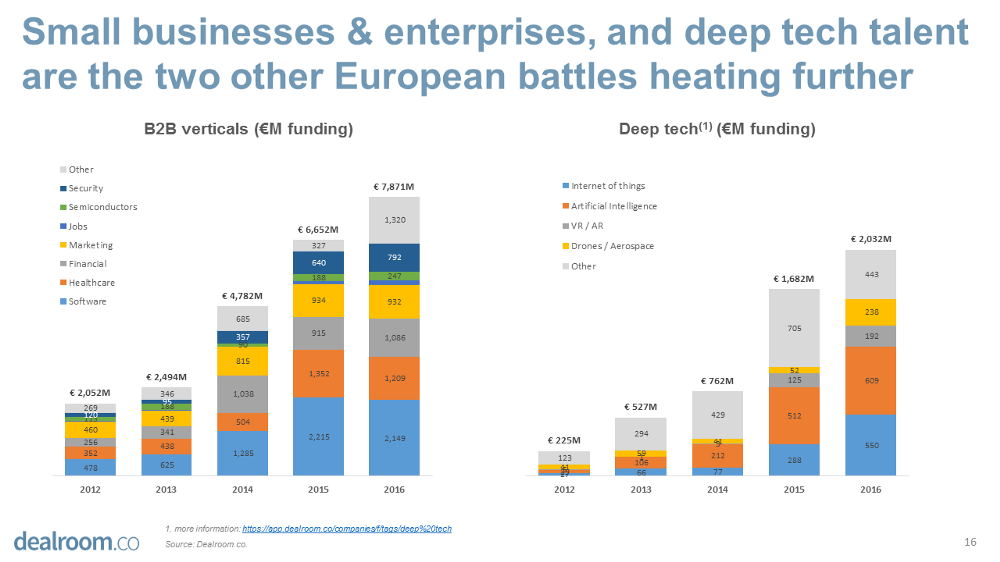

Insight #8: Deep tech investing grew 10x during last 5 years, to € 2 billion

2016 saw a continued rise in investment activities in deep tech such as artificial intelligence, virtual/augmented reality, robotics, drones, aerospace, and other so called deep tech segments. An important milestone was Atomico’s € 10 million investment in Lilium Aviation (yes, flying cars).

The battle for the small business and enterprise users is also likely to heat up during 2017. Growth areas included: security, B2B fintech, and marketing tech.

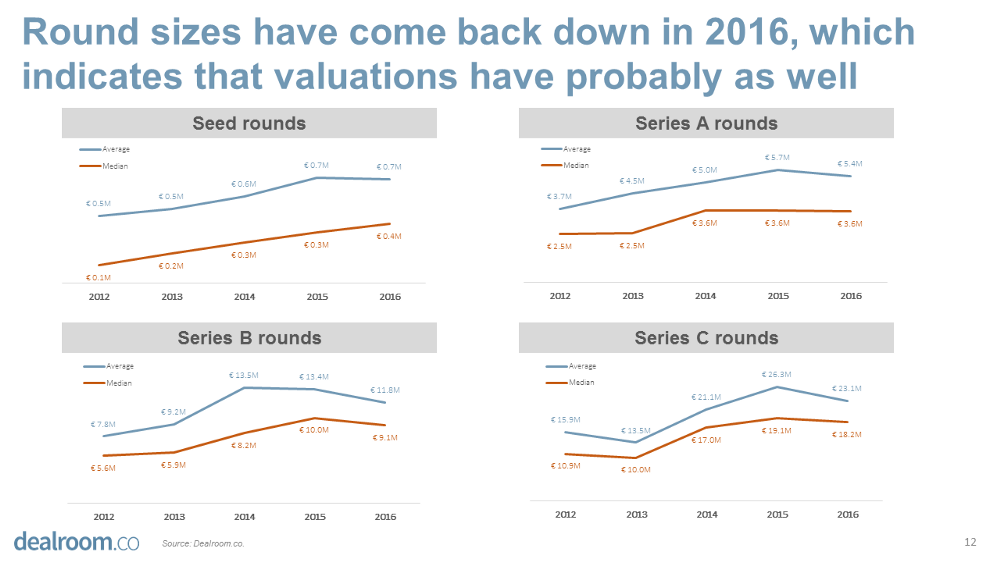

Insight #9: During 2016, valuations have normalised

Accurate information about valuations is hard to obtain (it needs to be based on a large enough random sample to be reliable). But total round sizes are a good proxy for valuation (the dilution per round is usually 20–25%). In 2016, rounds sizes of series A, B and C have come back down from their peak in 2015, in 2016 to 2014 levels, which could be a good sign for the long-term health of the VC ecosystem.

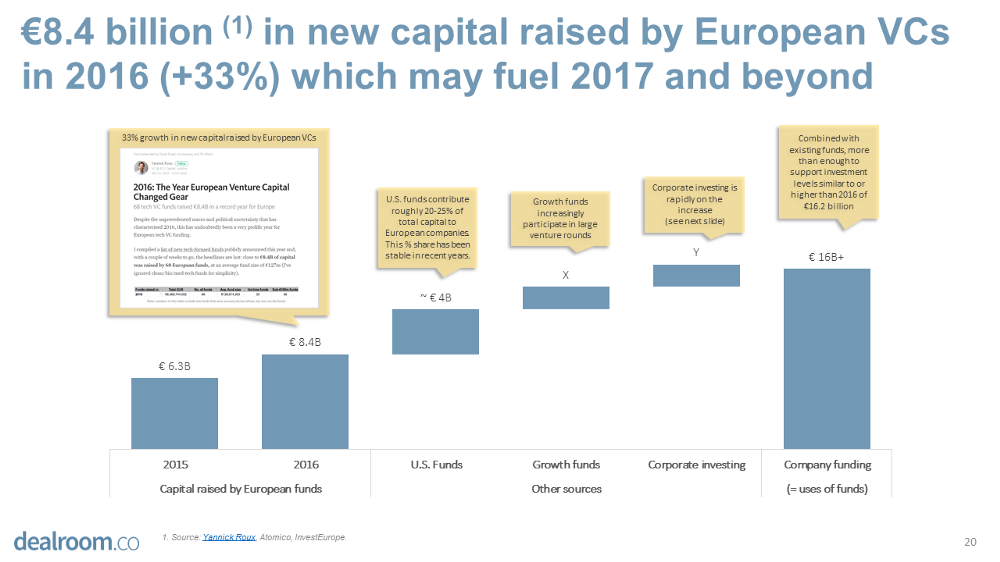

Insight #10: European VC funds raised well over € 8.4 billion in new funding from LPs

European VCs raised well over € 8.4 billion in new capital in 2016, an increase of +33%. New investment funds were raised across Europe, with Germany, the UK, France, and Netherlands in the lead.

This increase in available funds is coupled with: increasing activity of corporate funds mentioned earlier, increasing involvement of private equity making growth equity investments, and U.S. funds’ increasing involvement in Europe. Combined, this provides ample firepower (capital) to fuel levels of VC activity beyond that of 2016.

Outlook for 2017

The fundamentals are in place for continued growth in 2017: more new capital raised by European VC funds, corporate involvement will likely increase even further, and U.S. investors will continue to be very active as well. How much capital is too much capital? In consumer tech we seem to have reached a (temporary?) cap, to some extent. But venture funding per capita is still only at about 1/10th of the U.S. level of investment in most parts of Europe, indicating there is still plenty of headroom left (provided that startups have big enough international ambitions).

With fast growth of capital available, there’s a risk investors lowering their quality standards by some participants. No doubt the European VC ecosystem still has to go through a learning curve and will experience a few bumps along the road. The real test will be: follow-on rounds, profitability and exits. It takes on average 18–24 months between rounds (from seed and series-A, from series-A to B, and so on), so we will see in 2017 and 2018 how the quality of the 2016 vintage compares to previous years. Sign up on dealroom.co if you’d like us to keep you posted on these developments.

*Yoram Wijngaarde is the Founder & CEO of Dealroom.co – data and research about high-growth companies in Europe and beyond.